Et une video intéressante sur la situation

Dans le domaine de la fibre optique qui est en pleine croissance tel que LTE.C soumis par Accumbens, je surveille VTI.V Valdor technologies qui a reçu un contrat de 1.1m avec son partenaire Mexicain Inteligencia et est en attente d’une réponse pour un bid de $10 million soumis a une compagnie de télécom Nord-Américaine.

2 « J'aime »

LTE devrait bien faire dans les semaines à venir

J’ai mis le lien dans PHM par contre il y a aussi un entretien avec le CEO de Canopy Growth Corp. un titre qui a été mentionné ici et qui peut en intéresser quelques-uns

Trading Halt pour Espial et on annonce un revenue record de 8.7 million, le titre a descendu fortement aujourd’hui pour remonter a la fin de la journée

Espial Group earns $2.2-million in Q3 2015

Les résultats pour le Q3 sont sortis :

VANCOUVER, Oct. 29, 2015 /CNW/ - Tinkerine™ Studios Ltd. (TSXV: TTD, FSE: WKN WB6B and OTC: TKSTF) (“Tinkerine” or the “Company”) is pleased to announce its financial highlights for the three and nine months ended September 30, 2015. The Company’s unaudited interim financial statements and management discussion and analysis (“MD&A”) for the three and nine months ended September 30, 2015 are available on SEDAR at www.sedar.com and on the Company’s website at www.tinkerine.com.

Highlights

Q3 2015 revenue of $465,780, a 370% increase from Q3 2014 revenue of $98,898.

Revenue of $919,308 for the nine months ended Sept. 30, 2015, a 284% increase over $239,157 for the comparative 2014 period.

Q3 2015 gross profit of $258,226, a 650% increase from Q3 2014 gross profit of $34,423.

Q3 2015 gross profit margin of 55% versus a gross profit margin of 35% for Q3 2014.

Continued to expand and strengthen the dealer network for our 3D printers and conducted the majority of sales through dealers in Q3 2015.

Net loss for Q3 2015 of $138,589, versus a net loss of $536,381 in Q3 2014.

Financial Summary

Q3 2015

Q3 2014

Nine months

2015

Nine months

2014

Revenue

$465,780

$98,898

$919,308

$239,157

Gross Profit

$258,226

$34,423

$452,458

$144,751

Gross profit margin

55%

35%

49%

60%

Expenses

$396,815

$570,804

$1,459,747

$1,282,472

Net Income (Loss)

($138,589)

($536,381)

($1,007,289)

($1,137,721)

To date in 2015 we have ramped up our sales each quarter through the expansion of our dealer network particularly in the United States and Canada. Additional efficiencies continue to be recognized as the manufacturing process is optimized by our production team. We also tightened controllable expenses and brought the Company well in the direction of achieving cash flow positive results.

Outlook

To continue to expand our sales channels, we are focusing additional efforts on extending our dealer networks internationally. Our dedication to integrating STEAM based (science, technology, engineering, arts and mathematics) education content with 3-D printing is the foundation of future sales growth. Tinkerine continues to devote resources to research and development which includes hardware advancements, our Tinkerine Suite software and Tinkerine U online content delivery platform.

1 « J'aime »

ESP va prendre une grosse débarque aujourd’hui on dirait. J’imagine que le marché s’attendait à plus

Pour Espial, le marché anticipait une entente avec rogers communications ce qui n’a pas eu lieu. Espial est en croissance et cap flow positif, Espial a 47 million en cash, soit environ $1.30 l’action, j’ai pas vendu mes actions aujourd’hui, je crois qu’il va y avoir une remonté puisque Espial pourrait sécuriser d’autre contrat d’ici la fin de l’année. Selon le rapport de Mackie Research, Espial pourrait être aussi une cible d’achat de Cisco.

Potential for transformative partnerships and take-out. Cisco, recently introduced the “Infinite” Suite of Cloud video solutions. Cisco’s Home solution features a “thin” client for user experience. We believe ESP could potentially partner with Cisco and may have already taken some initial steps in this regard, which could be a major positive catalyst for ESP stock. We note Cisco divested its STB unit in July to Technicolor for US$600 mln in cash and stock and is focusing on software and cloud centric solutions. As the STB industry evolves to place more emphasis on STB software vs. hardware, large STB makers such as Cisco, Samsung, Arris could acquire Espial in order to offset hardware headwinds.

Espial’s long-term prospects remain excellent despite setback, says Haywood

OGI à très bien réagi, mais très spéculatif.

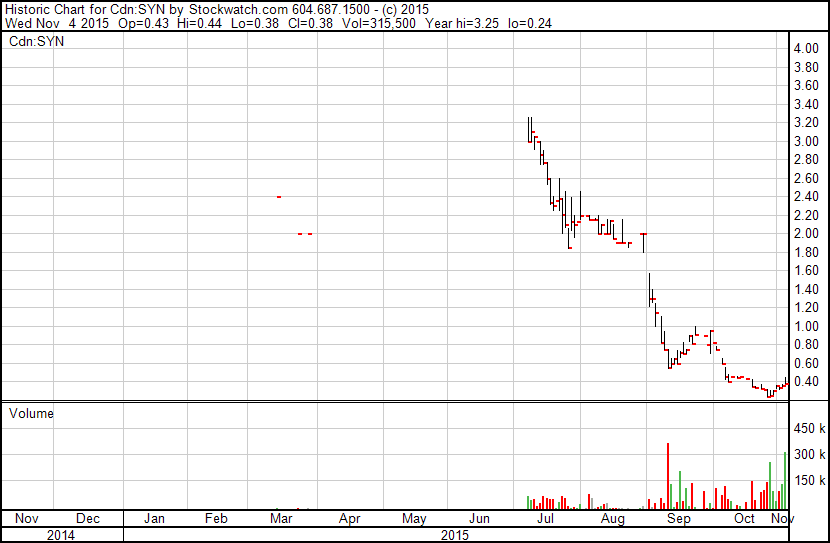

Un titre qui a retenu mon attention aujourd’hui SYN-V (SYNCORDIA TECH AND HEALTHCARE SOLUTIONS) , Du coté technique, il semble avoir une remonté du prix de l’action avec beaucoup de volume. Apres une courte vérification diligente, cette compagnie a un modèle d’affaire SaaS, en gros, elle s’occupe de la facturation pour les médecins, pour se faire rembourser pour les services fournis. Cela peut être un complexe, d’efforts coûteux en temps et très difficile à faire correctement. Leurs solutions aident à améliorer ces processus.

Prix de l’action aujourd’hui $0.38,

19.6 million d’actions en circulation

Voici leur présentation pour les investisseurs

Voici une analyse de Mackie avec un target a $2

Mackie began coverage on shares of Syncordia Techlgs&Healthcare Slutns Corp (CVE:SYN) in a research report issued on Thursday, StockTargetPrices.com reports. The firm set a “speculative buy” rating and a C$2.00 price target on the stock.

A number of other equities research analysts have also recently commented on SYN. Laurentian Bank of Canada initiated coverage on shares of Syncordia Techlgs&Healthcare Slutns Corp in a research report on Wednesday, September 2nd. They set a “buy” rating and a C$3.25 price objective for the company. LB Securities lowered their target price on shares of Syncordia Techlgs&Healthcare Slutns Corp from C$3.25 to C$2.00 and set a “buy” rating for the company in a research note on Thursday, September 3rd.

Syncordia Technologies and Healthcare Solutions Corp, formerly LL Capital Corp, is a Canada-based technology enhanced revenue cycle management (CVE:SYN) company. The Company is focused on various segments of healthcare, such as emergency medical services (EMS) and behavioral health. The Company is focused on investing in, partnering with and growing RCM companies. The Company has operations in North America and Europe. The Company is engaged in acquiring medical billing companies and in building a suite of RCM software solutions, the Syncordia Cloud. The RCM solutions include patient scheduling, electronic health records, claims management and analytics, among others. The Company’s wholly owned subsidiary is 9339639 Canada Limited.

2 « J'aime »

Titre intéressant, je vais faire mes recherches. Merci

Oui c’est sûr que c’est spéculatif dans une certaine mesure, mais l’air du temps, si tu me permet, est à ouverture de ce créneau a des fins récréatives et vu les promesses électorales du gouvernement Libéral, plusieurs investisseurs croie en une ouverture de ce marché, qui passera de moins 1 million de consommateurs à un bassin de 25,6 millions de personnes majeures au Canada. La question majeure est de savoir quand le marché va s’ouvrir.

Une compagnie québécoise offre le meme genre de service: Agyl MD

D’ailleurs la compagnie qui possède Agyl MD est en train de finaliser son RTO afin de devenir publique: Corporation de Capital de Risque Woden : Acquisition d’Happy Logic

AgylMD c’est pour le Québec seulement.

SYN-V a une valeur boursière d’environ $7M présentement et a plus de $10M en cash, je pense qu’il vont s’en servir pour faire une autre acquisition. J’aime aussi l’équipe de direction avec beaucoup d’expérience tel que Michael Plotkin qui a travaillé avec Steve Jobs comme directeur du développement web chez Apple / NeXT. Aussi les fameux Warrants dans le dernier PP ont un prix d’exercise a $3.30

1 « J'aime »

Signal d’achat à 0.54$ avec gros volume !

À noter qu’il y a 12M$ de notes payables au passif.

C’est toujours un défi de suivre une compagnie dont la stratégie est de croître par acquisitions. Il faut souvent se fier aux projections du management pour les résultats financiers futurs (synergies) et s’assurer que la structure financière de la compagnie (bilan) est adéquate pour soutenir une telle stratégie. Et bon quand une compagnie enchaîne les acquisitions, l’intégration peut être tout un défi. J’ai remarqué que si ç’a ne va pas comme prévu, les signes avant-coureur sont difficiles à identifier… On va toujours se baser sur les projections du management pour les résultats futurs (le prochain Q ou la prochaine année) jusqu’à temps que le bilan implose (ex: Loyalist Group). Quoique un facteur à considérer pourrait être: est-ce que le management a rempli ses promesses par le passé?

Pour revenir à SYN, je suis quand même intrigué par la compagnie. Le titre se transige à 1/3 de la valeur comptable et le domaine d’activités est intéressant. Je vais faire un peu de recherches cette semaine.

1 « J'aime »

Le 12 M$ de dette provient de Dean Knight income fund dans ce document que j’ai trouvé sur le net a la page 3

On November 5th, we structured a $12 million Secured Note ($3 million in the DK Income Fund) with Syncordia Technologies & Healthcare Solutions, Inc. Syncordia is a medical billing company looking to make acquisitions in a fragmented industry and improve the revenue cycle for its clients. The CEO, Michael Franks, successfully rolled up a number of small businesses in the non-emergency ambulatory transport industry. In the course of doing this, he identified an opportunity in medical billing as operators were not adept at navigating their way through the complicated claims process both at the government and insurance level. The medical billing industry itself is inefficient and Mike and his team identified areas, particularly through the development of software, to improve the revenue management cycle.

We are providing debt financing to help Syncordia make their first major acquisition, which is particularly attractive as the acquired company has a 14-year track record and has developed its own software which Syncordia can use in future acquisitions. The business they are acquiring has roughly $3 million in EBITDA and the purchase price of the business is $22 – $24 million, dependent on the company meeting performance covenants. Previous management had very good relationships with their two large customers but had never really developed a sales force. Syncordia’s team will bring their expertise to the business and grow it through an internal sales force, and by acquisitions.

In addition to the $12 million in Notes, the company has raised over $15.5 million in equity, with significant insider participation. Our Notes have security over the business, their IP, and any future acquisitions. The debt has a term of 3 years, paying a commitment fee of 2% and a coupon of 11%. In addition, noteholders receive 125 warrants per $1,000 of Notes with an exercise price of $2 per share, a 25% premium to the company’s concurrent equity raise.

1 « J'aime »

Je viens de prendre une énorme position dans UWTI. Je vois le pétrole à un plancher présentement et UWTI pourrait s’apprécier de 20% à 30% à très court terme ( 5-10 jours ) si ma prédiction s’avère vraie. J’ai embarqué sur marge à 8.80$ et je prévois en rajouter si ca baisse plus

Sur quoi tu te bases